Auto Loan Calculator

Calculate payments over the life of your Loan

Home Blog Privacy Terms About ContactCalculate payments over the life of your Loan

Home Blog Privacy Terms About ContactPublished on October 15, 2025

My learning journey started not with a grand financial plan, but with a simple, nagging question sparked by two numbers on a screen. I was exploring some online tools, just out of curiosity, and I put in a hypothetical personal loan amount of $13,850. The tool then presented me with a few repayment scenarios, and two of them caught my eye: a 36-month option and a 60-month option.

The 36-month plan had a monthly payment of around $430. The 60-month plan, however, had a monthly payment of just over $274. My immediate, gut reaction was one of relief. The lower number felt so much more manageable, so much less intimidating. Why wouldn't someone automatically choose the option that puts less strain on their monthly budget? It seemed like a no-brainer.

But then, a second thought crept in. It felt too easy. How can paying less each month for the same amount of money be the better path? What was I missing? Was there some hidden mechanism at play that I just wasn't seeing? This wasn't about making a decision; it was pure curiosity about the math itself. I wanted to understand the mechanics behind those two numbers and see how they related to the total amount I would theoretically repay. My goal was simple: to peel back the layers and understand the relationship between the length of a loan and its ultimate numerical footprint. This is purely my journey to understand how the calculations work, not financial advice.

I decided to spend some time with online calculators, not just to get an answer, but to truly understand how they arrived at that answer. I wanted to see the numbers move and react as I changed the inputs, hoping to uncover the logic that seemed to be hiding in plain sight.

My first attempt to solve this puzzle was, in hindsight, quite naive. I figured I could just do some quick "back-of-the-napkin" math. My mistake was in how I thought about interest. I had this vague idea that interest was just a percentage of the original loan amount, tacked on at the end. I wasn't really considering the element of time in a meaningful way.

So, I looked at the two scenarios for the $13,850 loan at a hypothetical 7.2% interest rate:

My flawed logic went something like this: "Okay, the monthly payment for Option B is much lower. The interest rate is the same for both, so the overall expense should be pretty similar, right?" I was so focused on that monthly payment figure that I mentally minimized everything else. I wasn't seeing the whole picture.

The real moment of confusion came when I finally used a proper online loan calculator and looked beyond the monthly payment field. I plugged in the numbers for the 36-month loan. The calculator showed a "Total Interest Paid" of around $1,616. That made some sense. Then, I changed only one thing: I switched the loan term from 36 months to 60 months. The monthly payment dropped, just as I expected. But then I looked at the "Total Interest Paid" field again. It didn't stay the same. It didn't even go up a little. It jumped to over $2,603.

I stared at the screen for a moment. I must have done something wrong. I re-entered the numbers. Same result. A loan with a lower monthly payment was resulting in nearly $1,000 more in total interest. The math wasn't behaving the way my intuition said it should. This was the reality check. My simple, static view of interest was completely wrong. I knew then that I didn't understand the fundamental mechanics of how loan repayment truly works over time.

The frustration of not understanding quickly turned into a determination to figure it out. The calculator wasn't broken; my understanding was. That's when I had my breakthrough. I stopped trying to guess the answer and started to use the tool as a learning device. The key was isolating the variables.

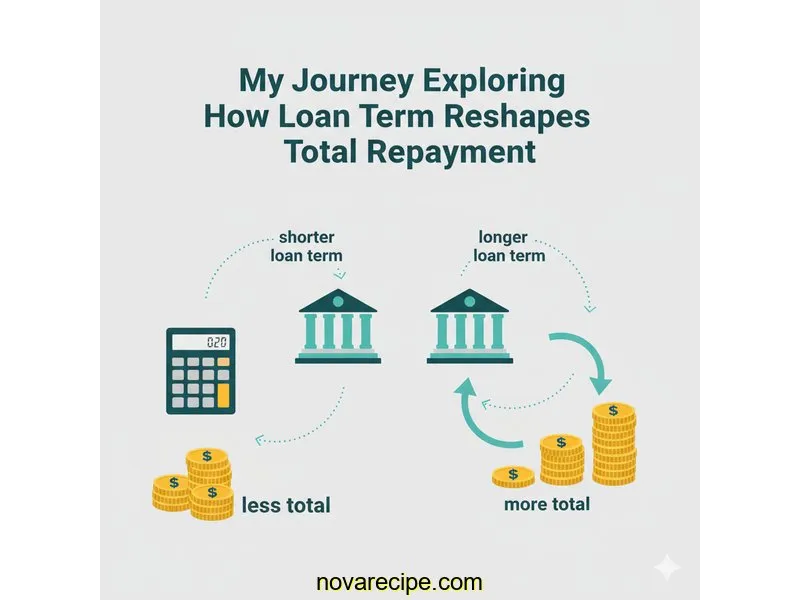

I kept the loan amount ($13,850) and the interest rate (7.2%) locked in. The only number I adjusted was the term, watching the other fields react. I slid the term from 36 months to 48, then to 60, then to 72. With each increase, I saw the monthly payment drop, which I expected. But I also saw the "Total Interest Paid" climb steadily higher. It was a direct, undeniable relationship. The longer the term, the more interest accumulated. The "aha" moment was realizing that interest is not a one-time fee; it’s a charge that's calculated repeatedly on the remaining balance. More time means more calculations, and therefore more interest.

I started digging into the "why." I learned that with each monthly payment, a portion goes to cover the interest that has accrued for that month, and the rest goes toward reducing the principal (the original loan amount). The interest for the month is calculated based on the current outstanding balance. On a longer-term loan, the payments are smaller, meaning a smaller portion of each payment is applied to the principal. This keeps the principal balance higher for a longer period, giving interest more time and a larger base to accrue against month after month.

The pure arithmetic finally clicked into place. It wasn't magic; it was just multiplication. For the 36-month term, the total repayment was $429.62 x 36 months = $15,466.32. For the 60-month term, the total repayment was $274.22 x 60 months = $16,453.20. Seeing the two totals side-by-side made it obvious. The longer term resulted in 24 extra payments. Even though each payment was smaller, those two extra years of payments were composed largely of interest, driving the total repayment amount significantly higher. The lower payment wasn't a discount; it was the result of stretching the same debt over a longer, more expensive timeline.

To be sure I grasped the concept, I ran more tests. I tried a different loan amount, like $21,500, with a different rate, like 5.9%. The pattern held true every single time. A 48-month term always resulted in less total interest than a 72-month term. This confirmed my learning: the term of a loan is one of the most powerful variables in determining the total amount of interest paid. It’s a fundamental lever in the machinery of loan mathematics.

This whole experience was incredibly illuminating. It was like learning the rules of a game I had only been watching from the sidelines. By focusing on just one variable—the loan term—I uncovered several core principles of how loan math works. My understanding shifted from a fuzzy, intuitive guess to a much clearer, logic-based comprehension.

The loan term directly determines the number of payments you will make. A longer term means more payments. Since each payment includes interest calculated on the remaining balance, more payments inevitably lead to a higher total interest paid, which in turn increases the total repayment amount.

The monthly payment is lower because you are spreading the repayment of the principal and total interest over a greater number of months. Think of it like slicing a pizza into 12 slices instead of 8; each slice is smaller, but the total amount of pizza remains the same (or in the case of a loan, actually grows larger due to the extra interest).

From a purely mathematical standpoint of understanding the overall expense, the "total interest paid" is an extremely useful metric. It strips away the principal and shows you the raw numerical expense of borrowing the money over different timeframes, allowing for a very direct comparison.

Find a reliable online loan calculator and enter a loan amount, interest rate, and term. Note the monthly payment and total interest paid. Then, without changing anything else, adjust only the term (e.g., from 48 months to 60 months). Observing how the other numbers change in real-time is one of the best ways to build an intuitive understanding of these mechanics.

If there's one thing I've taken away from this deep dive, it's that the numbers on the surface don't always tell the whole story. My initial assumption that a lower monthly payment must be "better" was based on an incomplete understanding of the mechanics at play. The real story was hidden in the dimension of time.

My biggest learning moment was realizing that online calculators are more than just answer machines; they are powerful learning tools. By isolating variables and observing the outcomes, I was able to teach myself a fundamental concept of personal finance math. It wasn't about finding the "right" loan, but about understanding the principles that govern all loans.

I hope my journey encourages you to play with the numbers, too. Ask questions. Use the tools available not just to get a result, but to understand the process. Building this kind of calculation literacy empowers us to see the full picture, and that's a valuable skill for anyone to have. I feel much more confident in my ability to understand how these financial instruments are structured, and that confidence came from simple curiosity and a willingness to explore.

This article is about understanding calculations and using tools. For financial decisions, always consult a qualified financial professional.

Disclaimer: This article documents my personal journey learning about loan calculations and how to use financial calculators. This is educational content about understanding math and using tools—not financial advice. Actual loan terms, rates, and costs vary based on individual circumstances, creditworthiness, and lender policies. Calculator results are estimates for educational purposes. Always verify calculations with your lender and consult a qualified financial advisor before making any financial decisions.